Introduction

Corporate compliance is not just about regulatory checklists anymore. It is also about the way corporations conduct their business in order to reduce potential risks, to make good choices when selecting business partners, and to retain a positive reputation over the long run. Corporate Compliance is mainly influenced by 2 concepts: KYC (Know Your Customer) and KYB( Know Your Business).

KYC and KYB are two different concepts that address two different risk areas, however they work together, and a solid understanding of both is necessary for organisations to conduct business in a regulated environment or in a digital or cross-border environment.

Why KYC and KYB Matter in Modern Compliance

Criminal activity in finance has also changed. Fraud, money laundering and sanction avoidance are typically not one-time events; rather, they are ongoing throughout business relationships. Criminal behaviour often travels between people and businesses and can be concealed by multiple levels of corporate ownership.

Regulators now expect organisations to prove that they:

- have a complete understanding of who their “customers” are, and

- have a thorough understanding of the businesses they partner with, and

- have the procedures and systems in place to continuously monitor both customers and business partners throughout their business relationship, not just during the process of establishing an initial partnership, which is generally done through a KYC process.

Being able to demonstrate the ability to meet these expectations creates business advantages for organisations; therefore, KYC and KYB are more than procedural steps, they are strategic tools for organizations.

Read: Seller Farming vs Cold Calling: Which Brings Better Listings

What Is KYC (Know Your Customer)?

Establishing KYC protocols requires that your clients’ identities be confirmed prior to allowing them access to financial services, financial platforms, or other sensitive transactions. KYC has three primary objectives:

- To verify the client’s identity

- To identify the client’s potential legal and regulatory risks associated with that identity

- To determine if the client is listed on any sanctions or watch lists

KYC is primarily focused on risk associated with a person’s identity, as the objective of KYC is to ensure that there is a legitimate and real person behind every account or transaction.

What Is KYB (Know Your Business)?

KYB is used to determine the risks presented by businesses rather than solely by individuals. Businesses may have complex ownership structures designed to conceal ownership, control or intent.

As with KYC, businesses must take into consideration the risk associated with Ownership and Control of Business Entities as well as Ultimate Beneficial Owners (UBOs) of those entities. Without knowing the identity of the UBOs, businesses run the risk of doing

KYC vs KYB: Key Differences

| Primary Focus | Individual identity | Corporate legitimacy and ownership |

| Who Is Verified | Customers or users | Businesses, directors, UBOs |

| Main Risk Addressed | Identity fraud | Hidden ownership, shell companies |

| Data Scope | Personal documents and screening | Registration data, ownership structure |

| Complexity | Moderate | High (multi-layered entities) |

| Ongoing Monitoring | Risk-based | Event-driven and continuous |

| Relationship | Standalone | Often includes KYC for owners |

This distinction matters because individual risk and structural risk are not the same, and ignoring either weakens compliance defenses.

Why Ultimate Beneficial Ownership (UBO) Is Central to KYB

The majority of the regulatory failures in KYB occur due to missing or outdated records of UBOs. UBOs are important because:

- Financial crimes are frequently perpetrated using nominee shareholders.

- Ownership of businesses can change, but the change is rarely published publicly.

- Indirect control creates regulatory liability.

Regulators are increasingly seeing poor UBO identification as a major compliance failure, rather than a simple oversight.

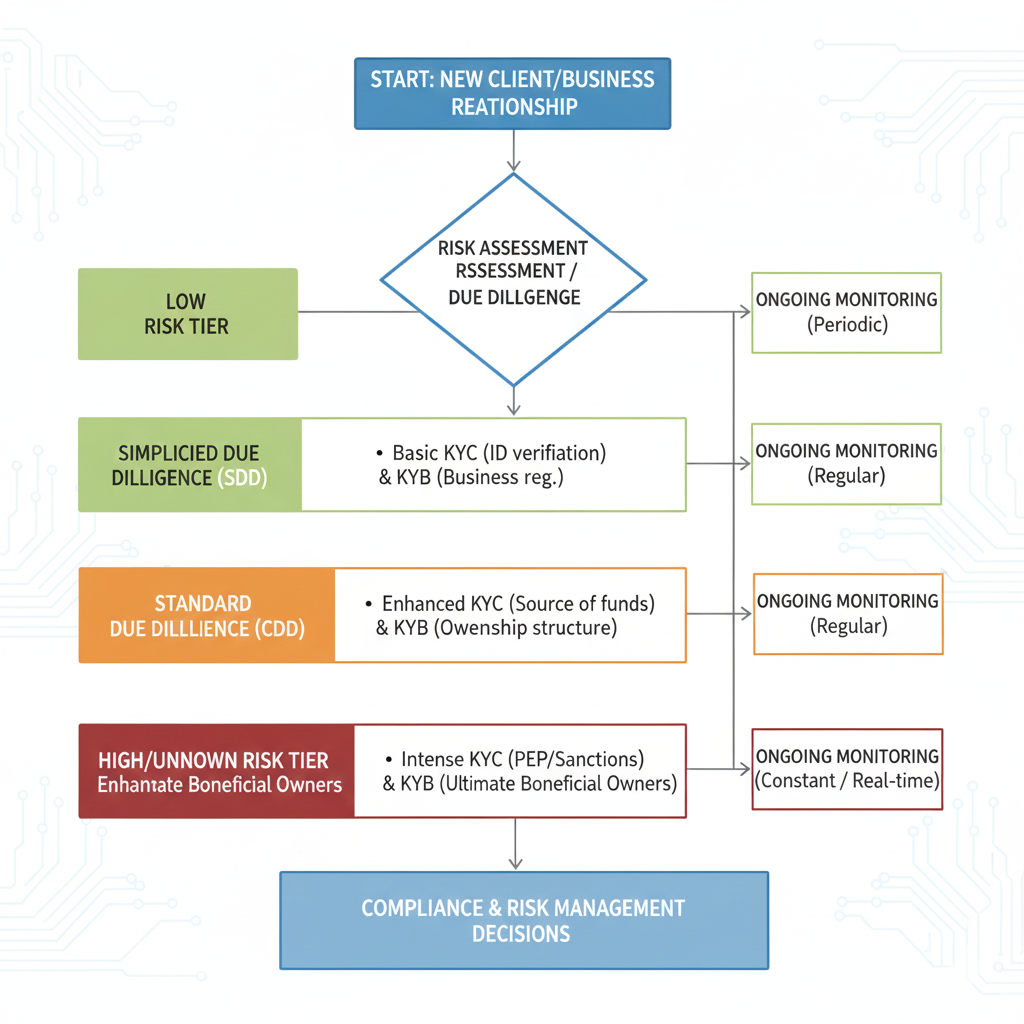

Risk-Based Compliance: How KYC and KYB Work Together

KYC (Know Your Customer) and KYB (Know Your Business) are two types of due diligence that are now required for every new business relationship, whether it is an individual opening a bank account or a company applying for credit; these processes have evolved over the past decade from being focused solely on the initial relationship (the application and opening) to now include ongoing monitoring for changes to risk.

Each of these 3 processes (KYC, KYB, and ongoing monitoring) should be treated separately when implementing an effective compliance program, as a regulatory imperative rather than simply ‘best practice.’

Initial Verification vs Ongoing Monitoring

A common misconception is that KYC and KYB end once onboarding is complete.

In reality:

- individuals change risk status

- businesses change directors, owners, and jurisdictions

Effective compliance programs separate:

- initial due diligence, and

- Ongoing monitoring, especially for KYB

This lifecycle approach is now a regulatory expectation, not a best practice.

Industry-Specific Compliance Expectations

Additionally, a variety of industries have different approaches to KYC and KYB, for example, merchants that accept payments through online marketplaces are now required to complete both KYC and KYB; similarly, in future technology companies and engagement platforms, it is critical that KYC and KYB are included as part of the same process, and; for B2B SaaS providers (Software as a Service), the vendor and partner function must undergo both KYC and KYB to reduce the risk of exposure from subsequent transactions.

Finally, as the way that business is conducted becomes more interconnected, the requirement for KYC and KYB will expand exponentially outside of what is currently mandated by the banking industry.

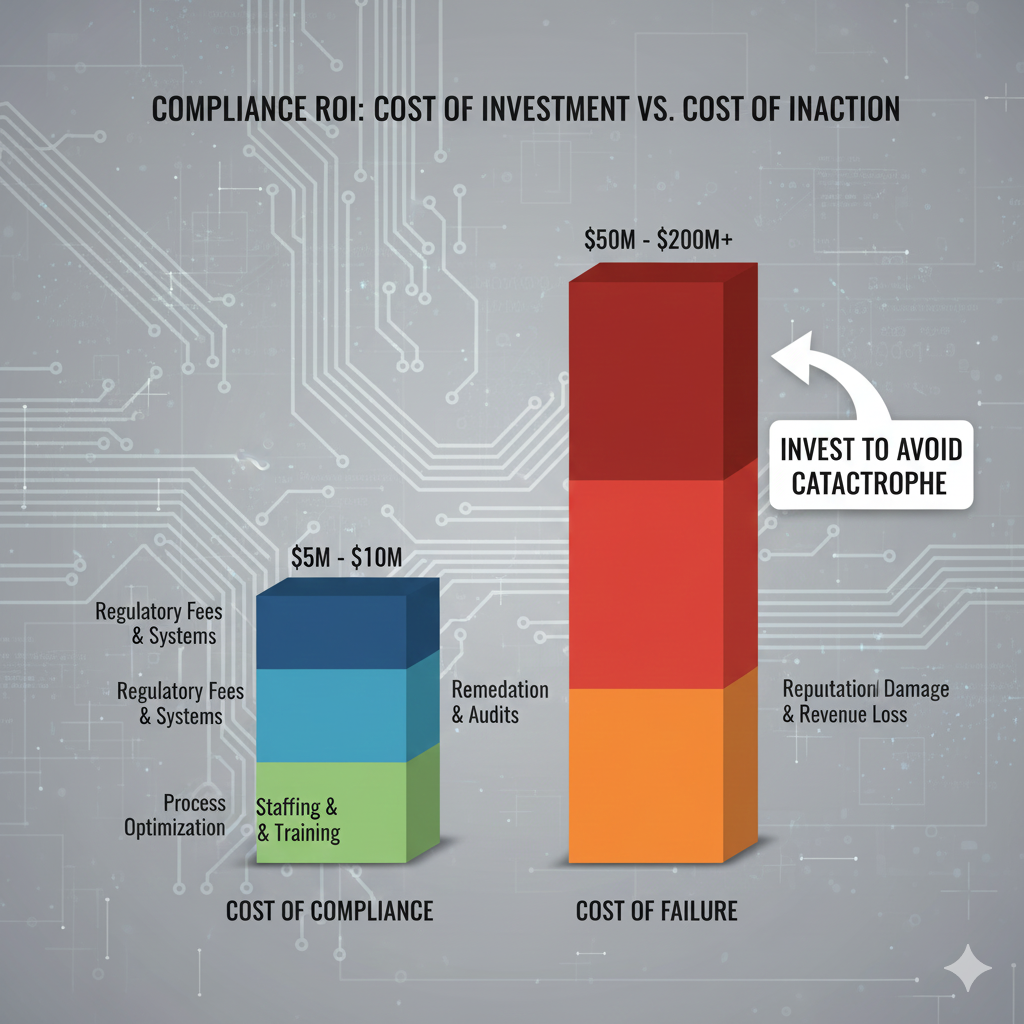

Cost of Compliance vs Cost of Failure

Compliance is often viewed as expensive, but non-compliance costs far more.

Risks of weak KYC or KYB include:

- regulatory fines

- forced remediation programs

- loss of banking partners

- reputational damage

When implemented strategically, especially with automation, KYC and KYB reduce long-term exposure and support sustainable growth.

Final Take: KYC and KYB as Strategic Assets

The real question is no longer whether companies need KYC or KYB.

It’s whether they understand how to integrate both effectively.

A robust KYC AML solution protects against individual misuse, while the KYB Business verification protects against hidden structural risk.

Together, they form the backbone of modern corporate compliance, supporting scalability, and regulatory resilience.

FAQs

Is KYB mandatory for all businesses?

KYB is required when organizations engage with other businesses in regulated or financial relationships.

Can KYB replace KYC?

No. KYB complements KYC but does not replace individual identity verification.

How often should KYB be updated?

Best practice is continuous or event-based monitoring when ownership or control changes.

Which is more complex, KYC or KYB?

KYB is generally more complex due to layered ownership and jurisdictional differences.

Author’s Bio:

Jeremy Blackburn is a veteran entrepreneur whose career spans mortgage banking, financial services, and breakthrough technology innovation. After founding ChainIT to apply blockchain-backed validation to commercial systems, he has continued to shape the industry with more than 30 patent filings.